While the current news cycle is dominated by the Iran war, one of the biggest themes shaping market narratives over the last year has been the impact of AI across different industries and the accompanying threat of job losses. Earlier this year, stocks in sectors like software and IT services took a beating as investors worried about AI’s potential negative impact. IT leaders like TCS and Infosys have seen their valuation multiples de-rate from a 2022 peak of 35x+ TTM P/E to 18x today.

The investing world is also seeing a rapid increase in adoption and usage of AI tools. We have had several conversations with fellow investors on how AI will change investing itself. In this letter, we explore the impact of AI on investing1 – what changes and what doesn’t?

What Changes?

In our view, for the fundamental investor, AI is primarily an efficiency and productivity play. It doesn’t change how we value a business, but it expands how much ground we can cover and how quickly we can cover it.

Traditionally, an analyst could gain an edge by being the first to “connect the dots” by studying financial statements, annual reports, investor presentations, earnings call transcripts and other regulatory filings. Today, LLMs and agentic AI tools can perform this task with remarkable speed and accuracy. AI can also build fairly accurate and detailed financial models. Information that took days to collate and analyze is now available in minutes. In short, a large part of what was considered skilled research work has been commoditized.

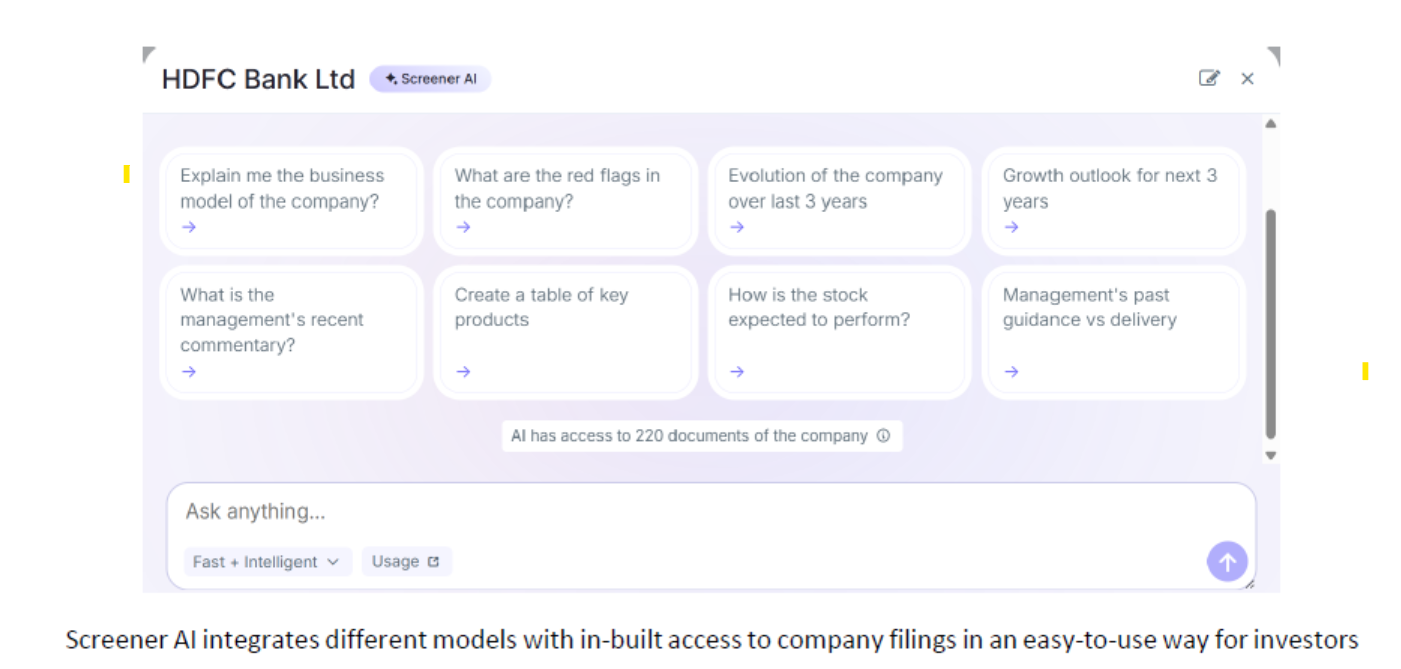

And the benefits aren’t limited to expert users of AI tools. Investing platforms are increasingly embedding AI into their workflows, lowering the barrier further. For example: Screener’s AI feature draws on a decade-plus of earnings call transcripts, annual reports, and investor presentations already housed in its repository, allowing investors to ask nuanced, multi-year questions without the need to upload a single document themselves. Similarly, Tijori Finance provides an AI-generated Guidance Adherence Check report which evaluates management delivery against past guidance. Until a few years ago, these activities consumed a lot of bandwidth and only the most diligent investors could perform these tasks. As AI models become stronger, more such tools will become available for investors to use in their research process.

At first glance, this might suggest that AI will enable investors to make better decisions and generate higher returns. In our view, the opposite is more likely because AI makes investing far more competitive than before. It reduces the gap between large institutions with extensive resources and the individual investor by democratizing both information and analytical ability. Previously, the labour-intensive process of fundamental research limited the investable universe for individual investors and small teams. AI reduces this bottleneck, allowing them to effectively compete even with large institutions2. As AI tools become stronger and usage becomes more mainstream, the alpha provided by an informational or analytical edge is likely to diminish. Much like the Red Queen Effect, investors will need to use AI simply to keep pace with the market and ensure they do not fall behind.

What Doesn’t?

While AI is largely commoditizing the “math” of investing, it doesn’t materially change a lot of the qualitative aspects of investing.

Garbage In Garbage Out

AI does not have its own investing philosophy or a belief system. It can either be a value investor or a momentum investor depending on what you want it to be. AI will faithfully follow your lead. If you lead it into noise, it will help you analyse noise with impressive rigour. Ask it about next quarter’s earnings and it will dissect every data point that bears on those earnings. If you lead it toward a signal, it will help you think about that signal with surprising depth. In a world where everyone has access to similar AI models, the differentiation shifts entirely to the quality of the prompts. And the quality of the prompts is a direct function of the quality of the mental framework you have. AI will not be useful if the basic investment philosophy itself is unsound.

AI Cannot Do Scuttlebutt

AI is good at synthesizing publicly available information and data. However, it cannot perform channel checks. A large part of the research process in small and mid-cap investing involves channel checks with industry experts, competitors, customers, ex-employees, etc. Just relying on the audited financials or management commentary to base your investment decision can be dangerous in the world of small and mid-cap investing.

For instance, a competitor could tell you that the company that you are evaluating is “stuffing the channel”, or an ex-employee could tell you that they were getting paid salaries in cash. AI cannot tell you this. On the other hand, AI will confidently tell you that a 50,000-crore market-cap company has ~40,000 outlets across India when the real number is less than 100. Or that a leading Housing Finance company has pristine asset quality and is available at throw-away valuations when, in reality, it’s a house of cards worth zero. Old-school on-ground research and channel checks would have easily identified these problems. AI cannot do the same as this information is not publicly available for the LLMs to digest. AI is unlikely to render the on-ground research aspect of investing obsolete.

Temperament and Conviction

The most important aspect of investing that doesn’t change is the relevance of temperament and conviction. The hardest part of investing isn’t calculating the intrinsic value, it’s having the stomach to hold or buy when the world feels like it’s ending (which seems to happen every few years). Even when broader markets are doing fine, outsized returns can be made by investing in sectors / companies that are going through a temporary period of pain (like Titan during demonetisation, or Nestle during Maggi crisis). Sound investing is also about resisting the temptation to invest during periods of euphoria (be it market euphoria or sector euphoria like Defence, CDMO, EMS, etc.) when FOMO hits hard. AI has little impact on decision-making driven by greed and fear.

We do not believe the rise of AI will change the cycle of boom and bust. This cycle is a fundamental characteristic of markets driven by human behavior. As more investors rely on AI tools, herd mentality could become even more pronounced because these models often react similarly to new data or news events. This shift might make human judgment even more important than before.

AI is definitely revolutionizing the process of how data is gathered and analyzed but the core tenets of value investing remain largely human. In a world of AI-generated research, the value of sound investing principles, deep channel checks, and a calm temperament will continue to remain high.

______________________________________________________________________________________________________________

1Our area of interest is only fundamental investing and not strategies like momentum, algorithmic, technical analysis or HFT.

2As a two-member investment team at 2Point2 Capital, this view may partly be driven by confirmation bias.